Blog

Special Reinvestment Allowance 2020

Overview of Special Reinvestment Allowance 2020

Manufacturing and agricultural company are eligible for Reinvestment Allowance(RA) as long as the companies incurred qualifying costs for qualifying projects.

So what is “qualifying cost” and “qualifying project”?

Key takeaways:

You will understand: -

1. Qualifying projects

2. Qualifying costs

Summary of learnings:

A) Qualifying Projects:

Qualifying projects are Expansion, Modernization, Automation and, Diversification. Let me explain by simple illustration as below: -

1. Expansion - Increase of a production capacity

Illustration:

i) Company A increased production from 12,000 units to 20,000 units per month.

ii) Company B is a manufacturer of rubber gloves, which goes into the manufacturing of cotton gloves. [similar products but different materials]

2. Modernization - Upgrading of manufacturing equipment and processes

Illustration:

i) Company C acquire new machines to cut down the number of processes, production time, and manpower.

3. Automation - Change manual operation into mechanical operation

Illustration:

i) Company D invested in a robotic arm for packaging which was done manually previously.

4. Diversification - Produce additional or new related products relating to the same industry

Illustration:

i) Company B, a rubber gloves manufacturer goes into rubber shoes.

[same materials but different products]

B) What is the Qualifying Cost?

Capital investment incurred for the “qualifying activity” is eligible for reinvestment allowance.

Two types of Qualifying Cost:

i) Factory: New / Extension of factory

ii) Plant and Machinery: New machines use in the production (replacement are not allowed)

Exemptions

- Capital cost incurred by the director, staff, or third-party usage is exempted.

- Capital cost which is not incurred for production purpose

- The company already enjoys other tax incentives. (Such as tax incentives from Promotion on Investment Act 1986, Investment Incentive Act 1968, Group relief or others)

Sources: - Reinvestment Allowances Part 1 – Manufacturing activity:

http://lampiran1.hasil.gov.my/pdf/pdfam/PR_10_2020.pdf

Stay tuned to our next ektp on “Requirements on documentations” and “Tax treatment” on Reinvestment allowance.

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

什么是 e-PCB ?e-Data PCB ?e-CP39 ?

什么是 e-PCB ?e-Data PCB ?e-CP39 ?

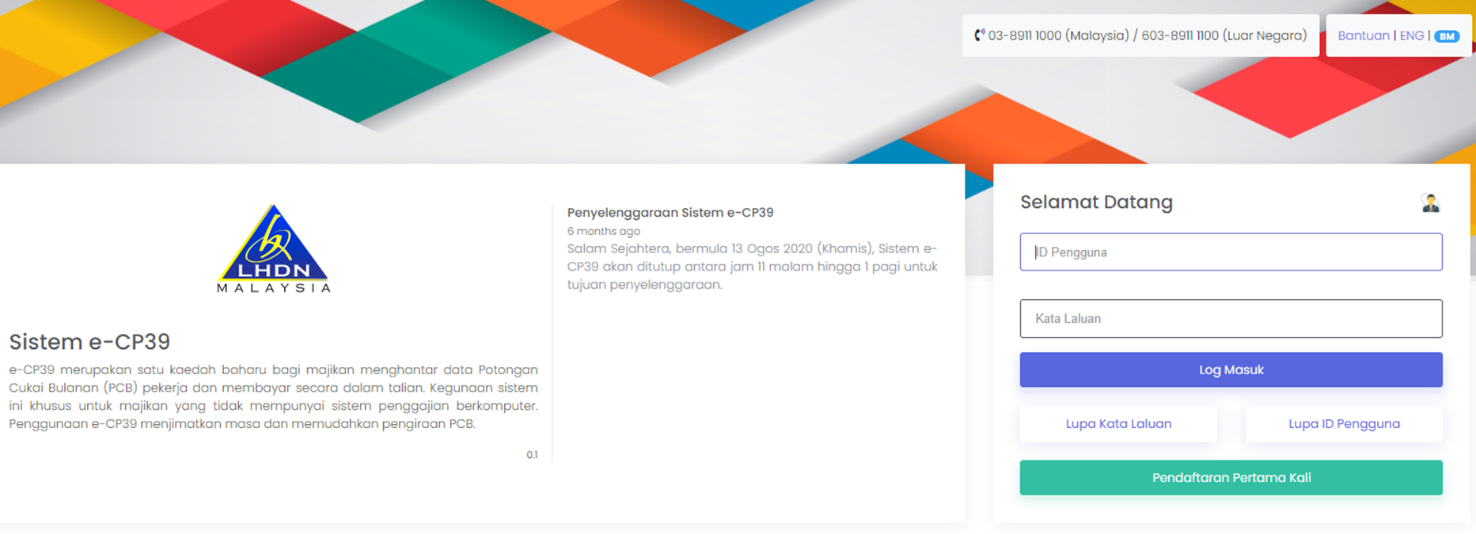

e-CP39

适合不需要每个月申报PCB的公司使用。无需申请账号亦可直接使用。

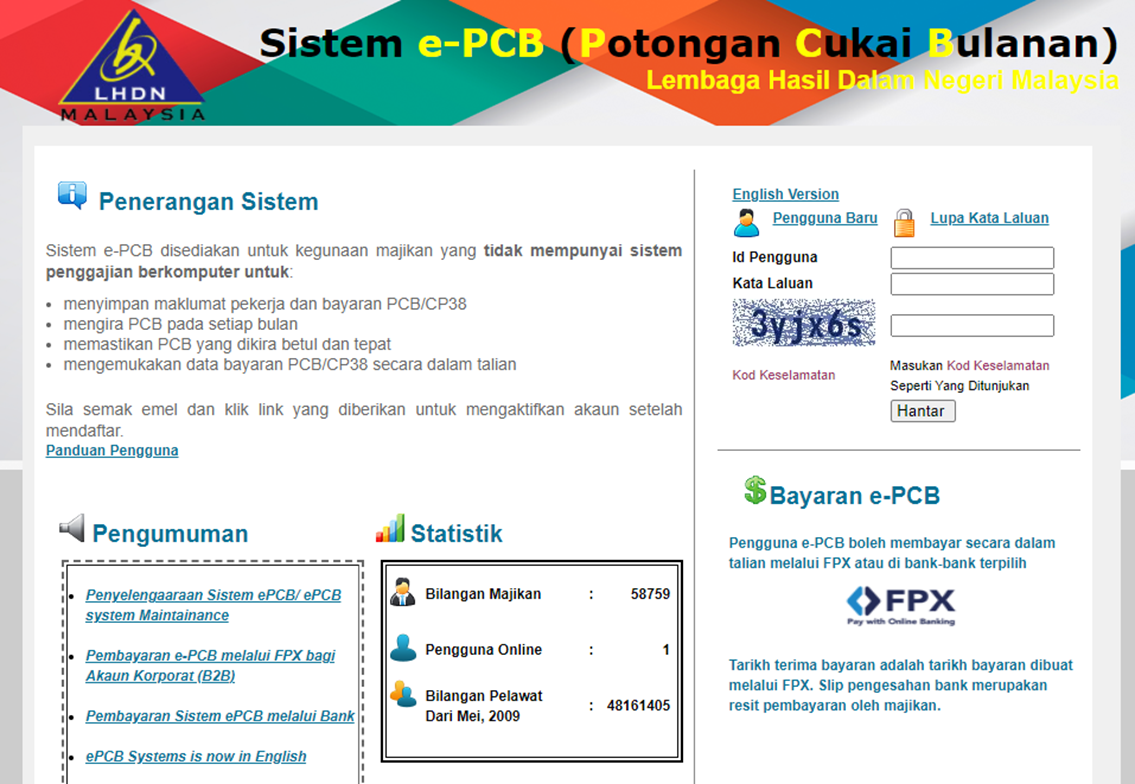

e-PCB

适用于没有薪资系统 (Payroll System) 的公司使用。雇主需要申请账号方可以此方式申报PCB。

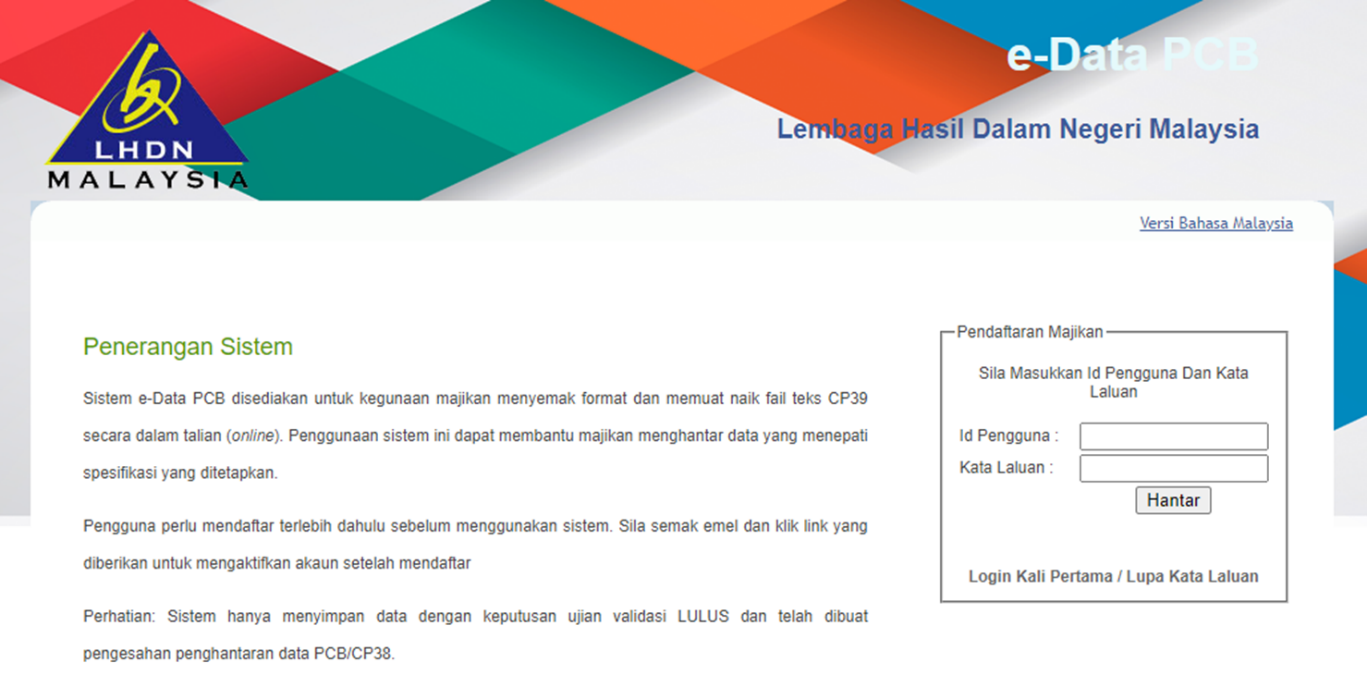

e-Data PCB

适用于有薪资系统 (Payroll System)的公司使用,通过薪资系统的PCB文档上载申报即可

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

What is solvency test in dividend distribution?

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

Real Property Gain Tax vs Income Tax on Gain on disposal of property/land

Gain on disposal of land – RPGT or Income Tax??

Let’s understand from a Real tax case: KST vs KETUA PENGARAH HASIL DALAM NEGERI

What is this case study?

KST sold a land to a developer company, amounting to RM1,520,000.00. IRB argued the disposal of land is subject to Income Tax Act 1967 (ITA).

KST did not agree

- Initial intention is to distribute land to 9 siblings and no intention for trade purpose.

- After that, KST dispose the land when KST received an offer from developer.

So, the gain from disposal of land is not subject to ITA1967.

What is IRB argument?

- The initial intention has changed.

- The holding period is short.

- KST is one of the director of land acquired company.

- Improvement on land is done before the disposal.

So, the gain from disposal of land is subject to Income Tax Act 1967 (ITA1967).

Decision by Special Commissioners of Income Tax:

Special Commissioner agreed with IRB tax treatment. Gain from disposal of land is subject to Section 4(a) ITA 1967.

What is the difference between RPGT and ITA?

The main difference is the “tax rate”. Let’s see the comparison as follows (tax rate for year of assessment 2020):

For individual (resident):

Income tax : Graduated rate from 0% to 30%

RPGT

- Disposal within 3 years from date of acquisition - 30%

- Disposal in the 4th years from date of acquisition - 20%

- Disposal in the 5th years from date of acquisition - 15%

- Disposal in the 6th years from date of acquisition - 5%

For company (resident)

Income tax

- 17% on the first RM600,000.00 of chargeable income*

- 24% on the subsequent balance of chargeable income

*Resident company with paid up capital of RM2.5 million and below at the beginning of the basis period and having gross income from source or sources consisting of a business not more than RM50 million for the basis period for a year of assessment.

RPGT

- Disposal within 3 years from date of acquisition - 30%

- Disposal in the 4th years from date of acquisition - 20%

- Disposal in the 5th years from date of acquisition- 15%

- Disposal in the 6th years from date of acquisition - 10%

How to determine the disposal is subject to RPGT or ITA?

The badges of trade should be considered:

- Method of acquisition of real property - How was the property acquired? For example, inheritance, through open market or auction.

- Nature of the real property - Whether the property is generating rental income or left for vacant?

- Number of transactions - Frequent transaction is likely to indicate trading of properties and subject to income tax.

- Profit seeking motive - Intention of making profit will be subject to income tax.

- The period of ownership - How long was the property held before disposal?

- Alteration, modification or improvement made to the real property - Renovation or improvement of property before disposal may be viewed as effort to enhance the value of the property, it may subject to income tax.

- Source of financing - How was the purchase of property financed? Short-term or long term borrowing?

- Circumstances surrounding the sale - What were the circumstances leading to the sales of property? Was the property sold because of realise profit or emergency need of funds?

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Shareholders' defence on excess distribution

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Who to recover the excess distribution

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Latest development on filing CP 21 & CP 22A online.

Latest development on filing CP 21 & CP 22A online.

Following our first sharing of E-SPC on CP forms on 19/1/2021, it appear some LHDN's branches in Malaysia

1️⃣Stop submission via E-SPC online

2️⃣Stop submission via email.

What is your current practice in your location? Care to share?

Look like LHDN mandatory choice of CP form submission over the counter physically.

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Tax incentive to cut taxpayer tax - Reinvestment Allowance Part 1

Reinvestment Allowance (RA) - Part 1

What is reinvestment allowance?

Reinvestment allowance (RA), as the name suggests, is an incentive to encourage companies to reinvest and expand their businesses. It is only granted after the company has been in business for a certain period of time, and only to companies resident in Malaysia.

How good is reinvestment allowance?

The allowance is given for 15 years from the first year of claim. The allowance is computed at 60% of QCE incurred and can be utilised against 70% of statutory income

Latest development in reinvestment allowance

Budget 2021 has announced that a special Reinvestment Allowance (RA) will be given for eligible manufacturing and agricultural projects in Years of assessment (YA) 2020 to YA 2022.

This means that eligible companies that have fully utilized their 15-years RA can enjoy additional RA claims for 3 years (YA2020 to YA2022).

Key takeaways:

-

What is Reinvestment Allowance (RA)?

-

Period of Eligibility

-

Conditions of Eligibility

What is Reinvestment Allowance (RA) for manufacturing?

Reinvestment Allowance (RA) is an incentive for manufacturing companies to encourage reinvestment or continued investment by foreign and domestic investors.

Period of Eligibility

The eligible company is entitled to claim RA for 15 continuous years.

Conditions of Eligibility

Manufacturing company has to meet the following criteria to be eligible for this allowance:

-

Operates in manufacturing business for at least 36 months.

-

Definition of manufacturing for the purpose of RA as follows:-

i. Conversion of organic or inorganic materials into a new product;

ii. Assembly parts into pieces of machine or products; or

iii. Mixing of materials by chemical reaction processes

This means that activities such as installation of machinery or simple operations that does not requires special skills or equipment are not considered as manufacturing in the context RA.

3. Company is a Malaysia resident (at least held one meeting of Board of Directors in Malaysia in the year).

-

Company has incurred capital expenditure on a factory, plant or machinery used in Malaysia for the purposes of a qualifying project in the year of tax claim.

So what are the projects that are qualified for this allowance?

Stay tuned to next week e-KTP for Reinvestment Allowance Part 2

Source LHDN Public Ruling 10/20 Reinvestment Allowance : PR10/2020

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Excess Distribution of Dividend

Do you know what is excess distribution in dividend under S 133 (1) of CA 2016?

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Sad as we are rejected on WSP 3.0

We are not happy with Wages Subsidy Program (WSP) 3.0

𝐎𝐮𝐫 𝐚𝐩𝐩𝐥𝐢𝐜𝐚𝐭𝐢𝐨𝐧 𝐟𝐨𝐫 𝐖𝐒𝐏 𝟑.𝟎 𝐢𝐬 𝐫𝐞𝐣𝐞𝐜𝐭𝐞𝐝 because staffs have 𝐫𝐞𝐬𝐢𝐠𝐧𝐞𝐝 (𝐧𝐨𝐭 𝐭𝐞𝐫𝐦𝐢𝐧𝐚𝐭𝐞𝐝) since WSP 1.0 and WSP 2.0

We understand one of conditions is to 𝐦𝐚𝐢𝐧𝐭𝐚𝐢𝐧/𝐤𝐞𝐞𝐩 𝐚𝐥𝐥 𝐬𝐭𝐚𝐟𝐟𝐬 𝐮𝐧𝐝𝐞𝐫 𝐖𝐒𝐏? But...If staff want to resign, what can we do?

𝐇𝐚𝐯𝐞 𝐲𝐨𝐮 𝐞𝐱𝐩𝐞𝐫𝐢𝐞𝐧𝐜𝐞𝐝 𝐬𝐮𝐜𝐡 𝐢𝐧𝐜𝐢𝐝𝐞𝐧𝐭? 𝐂𝐚𝐧 𝐰𝐞 𝐚𝐩𝐩𝐞𝐚𝐥?

Background of WSP 3.0

WSP is back, are you eligible to apply?

Budget 2021:

- Tourism and retail industries only

- Date of application: 1st Jan 2021 - 30th June 2021

-

Period of subsidy:

- Existing applicant 3 months

- New applicant: 6 months - Subsidise amount: RM600 per employee with salary under RM4,000

PERMAI:

- Open to all industries in states in MCO

- Date of application: 19th Jan 2021 - 30th June 2021

- Period of subsidy: One month

- Subsidise amount: RM600 per employee with salary under RM4,000

Condition of WSP 3.0:

- Company have to apply thru SOCSO website

- Only for Company with revenue reduced by 30%

- Company is registered with SOCSO or PERKESO before 1/1/2021

- Up to 500 employees (based on size of entity) can be claimed for WSP3.0

- If employees resign voluntarily, Company only need to update the list of employee before 15th of the month

Entity size under WSP 3.0

- Below 75 employees (Number of limit which can claimed : 75 employees)

-

76 to 200 employees (Number of limit which can claimed : 200 employees)

-

More than 200 employees (Number of limit which can claimed : 500 employees)

Source of WSP 3.0

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP

#thk

#Wsp

#sosco

Impropoer & unlawful in dividend distribution

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

𝐊𝐓𝐏

Latest update on accounting for lease

The development on accounting for lease

Effective from 1 January 2019, IAS 17 Leases will be replaced by MFRS 16 with the following changes.

- The leases are no longer classified into operating leases or finance leases

- All leases are capitalised by recognising a lease liability and the right to use of assets on balance sheet.

This means that the Company which takes up leases that only allows the right of use of asset, and not the ownership of assets, will also need to recognise its right to use the assets (Asset) first, and later on expense off to the interest (Expenses) and depreciation of the assets (Expenses).

This affects the balance sheet of the company as the old accounting standards only requires Company to disclose these leases on the profit and loss.

The new standard on MFRS 16 and the effect on financial statements are as follows:-

- A ‘right-of-use’ model replaces the ‘risks and rewards’ model.

- Lessees should recognise an “right-of-use” asset and lease liability based on the payment under lease

- The lease liabilities must be measured to the lease term (optional lease period)

-

Lessees should reassess the lease term only upon the occurrence of a significant event or a significant change in circumstances that are within the control of the lessee

Double entry of accounting for leasing

For leases that allows right of use but the lessee does not have ownership at the end of the lease(i.e. renting an asset), the new accounting standard requires Company to recognise the lease on the assets and liability on balance sheet. So, at the commencement of lease, based on the contract of rental, the lessee will need to present the contracted rental payment as follows:

- Dr Right of use of asset

- Cr Lease liability

The asset and liability will be slowly reduced when the payment are made, as the company will expense off these expenses to profit and loss (i.e. interest paid, rental expenses/depreciation).

- Dr Lease liability

- Dr Interest paid

- Dr Rental expenses paid

- Cr Cash at bank paid

- Cr Right of use of assets

Recognition of lease

To recognize the right of use and lease liability by:

Right of use – measured by cost /fair value/ revaluation method

- obtain substantially all of the economic benefits from the use of the identified asset throughout the period of use

- direct the use of the identified asset throughout that period

Lease liability – Lessee needs to recognize on interest of lease liability

- there is an identified asset

- has the rights to all of the economic benefits from that asset

- directs the use of that asset, including how and for what purpose

Exemption

There has two specific exemptions where leases do not need to be reported on balance sheets:

- Leases with a term of 12 months or less with no purchase option

- A lease where the value of the item is low value.

Sources

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#accountingstandards

#mfrs16

#masb

What is MyTax from LHDN Malaysia?

What is MyTax App? 你知道什么是“MyTax”吗?

Ms C (Tax Agent):

我知道!这是一个方便纳税人查看税务的软件。你就可以查询并使用更多相关的税务服务。只要点击分类账, 你就可以查询自己有没有拖欠的税务. 并查询有关的税务估算表(CP500)。

I know! This apps is for taxpayer to check on their tax details. Click the “Favourite Service” to get more functions.

You can check any tax overdue by clicking on the “ledger” or check on your CP500 details.

Question : 这个软件有什么好处呢? Is this app good to use?

-

纳税人能更方便的查询个人的税收信息。

Easy for taxpayer to check on their own tax details

-

节省时间,成本和交通,无需去LHDNM柜台询问税收信息,因为一切都触手可及

Save time, cost and movement as taxpayer no need to visit LHDNM office to check the tax information

-

允许用户使用一个用户名(ID)和密码登录到多个相关软件系统,并使用LHDNM所提供的其他服务。

Allows taxpayer to use single ID and password to login and access difference LHDNM systems and services provided

Question : 怎样下载MyTax?How to download MyTax?

-

安卓用户可以通过 google play store下载 + 苹果用户可以在 app store下载

Android or IOS user can download the apps from either google play store or app store

Source: MyTax official website

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Solvency Test in Dividend Distribution

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

- Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

- Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏

- Website www.ktp.com.my

- Instagram https://bit.ly/3jZuZuI

- Linkedin https://bit.ly/3sapf4l

- Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

- Tiktok http://bit.ly/3u9LR6Q

- Youtube http://bit.ly/3ppmjyE

- Facebook http://bit.ly/3ateoMz

- Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

- Instagram https://bit.ly/3u2PxHg

- Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

- Website www.thks.com.my

- Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Dividend distribution : Steps

Do you know the steps on dividend distribution under S132 of CA 2016?

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Form EA 有什么?

Form EA 有什么?

Part A - 雇员的资料

-

姓名

-

工作职位

-

工作编号

-

IC号码

-

EPF 号码

-

加入日期和辞职日期(如果少于一年)

Part B - 就业收入,福利,住宿

-

收入

-

拖欠收入 (payment in arrears)

-

福利价值

-

住宿价值

-

未经’批准’的EPF或退休金退款

-

失业赔偿

Part C - 退休金

-

退休金

-

年金 (annuity)

Part D - 扣除总额

-

预扣税金

-

年金 (annuity)

-

CP 38 扣款 (税收局向积欠税款的纳税人雇主,发出“扣除工资令)

-

伊斯兰援助金 (Zakat)

-

员工通过表格TP1扣除的回扣金额

-

孩子回扣金额

Part E :Approved 退休金或公积金、基金或社团的缴纳总额

-

EPF

-

Sosco

Visit US

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

KTP Lifestyle (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career (Our job platform for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

THK (Our associate in secretarial & accounting services)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Medical Fee on director is a tax exempted BIK?

Under section 13(1) b Income Tax 1967, medical and dental benefits are exempted from income tax for employee?

But

Questions :

- Director of the control company = an employee of company for tax purpose?

- Does the exemption extend to directors of a controlled company like for any other employees of the company?

Under paragraph 8.3.1 , if the employee receiving BIK from the employer has control over his employer (company) is no exemption.

What is control?

For a company, the power of an employee to control is through :

- The holding of shares or

- The possession of voting power in or

- By virtue of powers conferred by the articles of association or other document.

What is control?

For a partnership, the employee is a partner of the employer.

For a sole proprietor, the employee and the employer is the same person

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Ask Secretarial : The basic requirement on dividend distribution

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Ask Secretarial : Non compliance on dividend distribution

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Latest update on CP 500

Overview of CP 500:

Every February or March of the year, the taxpayer shall receive the CP500 from LHDNM through post or email notification.

CP500 is a tax instalment scheme issued by LHDNM to individual taxpayer who carrying business income. For example, sole-proprietor, self-employed, partnership, person who received rental income or royalties.

Key takeaway:

You will understand:

a) What is CP500?

b) What is the due date for CP500?

c) What is the penalty for late payment on CP500?

d) Can taxpayer do revision for CP500?

e) Any penalty for revising CP500?

Summary of Learning

a) What is CP500?

This is the tax instalment issued by LHDNM for individual taxpayer who has income other than employment income such as business income, rental income and royalties.

If you not yet receive the letter by end of March, you may visit the tax office or contact LHDNM for more details.

However, taxpayer may not receive the CP500 if the taxpayer is making losses in last two years or just commenced the business.

b) What is the due date for CP500?

The tax estimate has to be paid bi-monthly in 6 instalments and the payment for each instalment should be made within 30 days from the date of payable (March, May, July, September, November and January).

c) What is the penalty for late payment?

If the taxpayer fail to make the tax instalment on time, LHDNM will impose a 10% penalty on the outstanding balance. The penalty is to be self-assessed and paid to the LHDNM.

d) Can taxpayer do revision for CP500?

Taxpayer is allowed to revise the CP500 by submitting Form CP502 to respective LHDNM Branch if they have any valid reason.

However, the revision must be submitted on or before 30 June of current year of assessment. LHDNM will issue the CP503X once they have approved for the revision.

e) Any penalty imposed for the revision?

If the revised tax payable (CP502) is 30% lower than actual tax payable, the difference will subject to a 10% penalty.

[(Actual tax payable – Estimated tax payable) – (30% x Actual tax payable)] x 10%

Sources:

CP502 Explanation Notes:

http://phl.hasil.gov.my/pdf/pdfam/CP502_NOTA_PENERANGAN_2.pdf

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firm which commit to help and grow our clients business.